The Roth Misunderstanding

Most people who argue about Roth vs. Traditional are working off bad math. And a lot of that bad math is being handed to them on purpose.

Start Here: The Same Spendable Principle

Here is the core concept, and I want you to sit with it before you keep reading.

If your tax rate is the same when you put money in as it is when you take money out, Roth and traditional produce the exact same spendable amount.

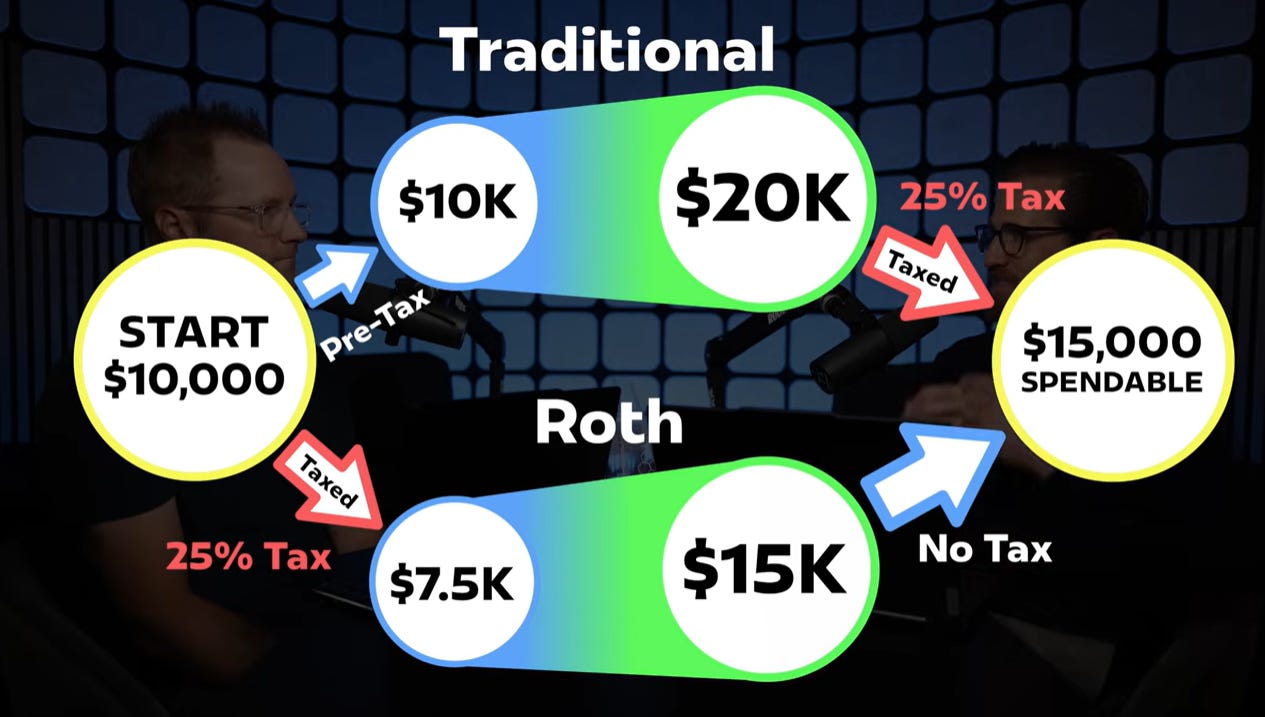

Let me show you the math. Say you have $10,000 to invest. You go the traditional route. No taxes now. It doubles to $20,000. You pay 25% on the way out. That is $5,000 in taxes. You walk away with $15,000 to spend.

Now go the Roth route. You pay 25% upfront. $2,500 gone. You invest $7,500. It doubles to $15,000. No taxes on the way out. You walk away with $15,000 to spend.

Same number. Every time.

This is what I call the Same Spendable principle. Once you understand it, the entire Roth conversation gets a lot clearer, because now you know exactly what you are solving for. The only thing that changes the outcome is a difference in your tax rate, now versus later.

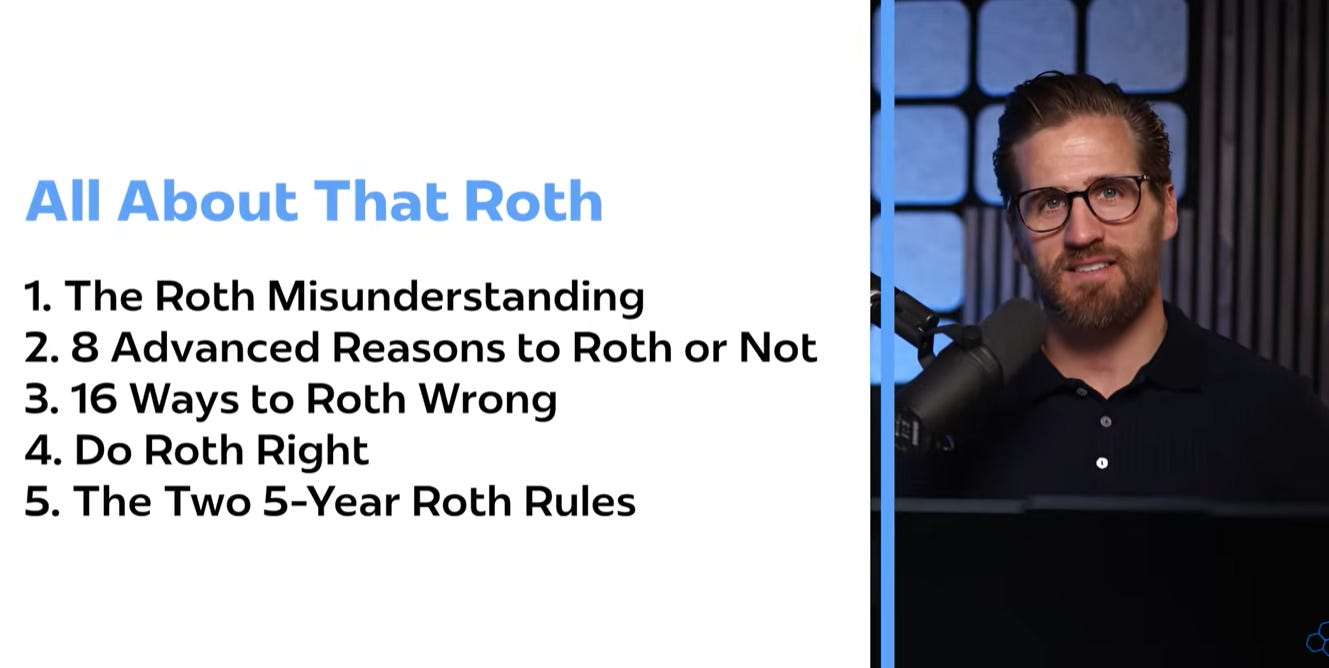

TOP 5 KEY POINTS in this post:

If your tax rate is the same going in as it is coming out, Roth and traditional produce the exact same spendable amount in retirement. Every time.

The only variable that actually matters in the Roth vs. traditional decision is whether your tax rate will be higher or lower in retirement than it is today.

You are being marketed to. Some advisors and financial personalities use fear about taxes to get you to act. The math is not that scary.

Maxing out your retirement contributions in Roth is worth more than maxing them out in traditional, because Roth dollars are 100% yours and traditional dollars are a partnership with the IRS.

Diversifying your tax status across Roth, traditional, and non-retirement accounts gives you degrees of freedom. That optionality is one of the most underrated advantages in retirement planning.

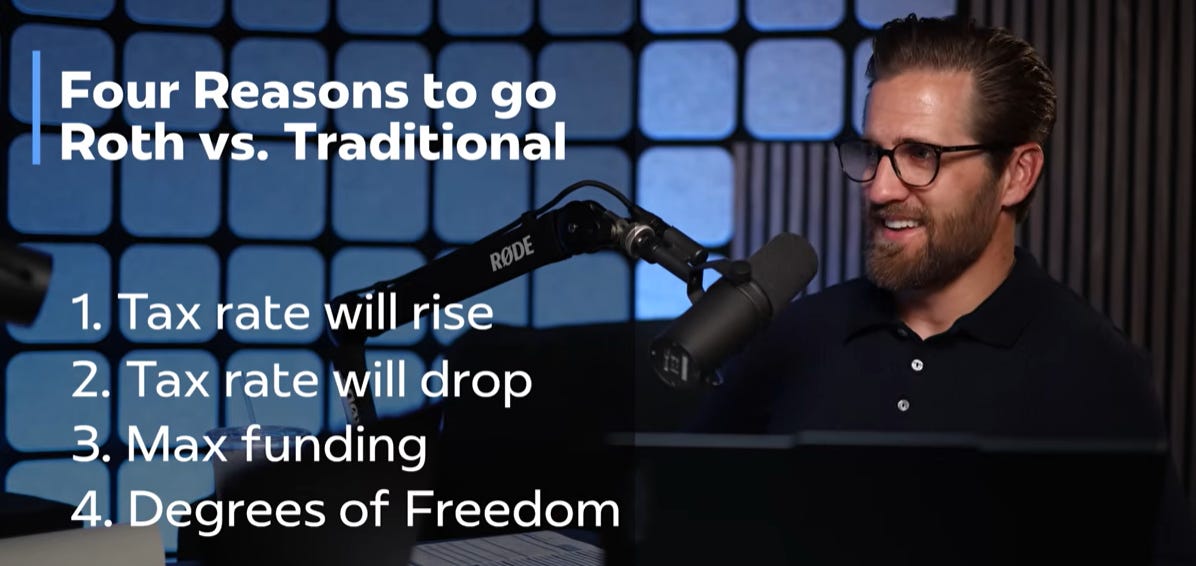

The Four Reasons to Go One Way or the Other

Everything comes down to four basic scenarios.

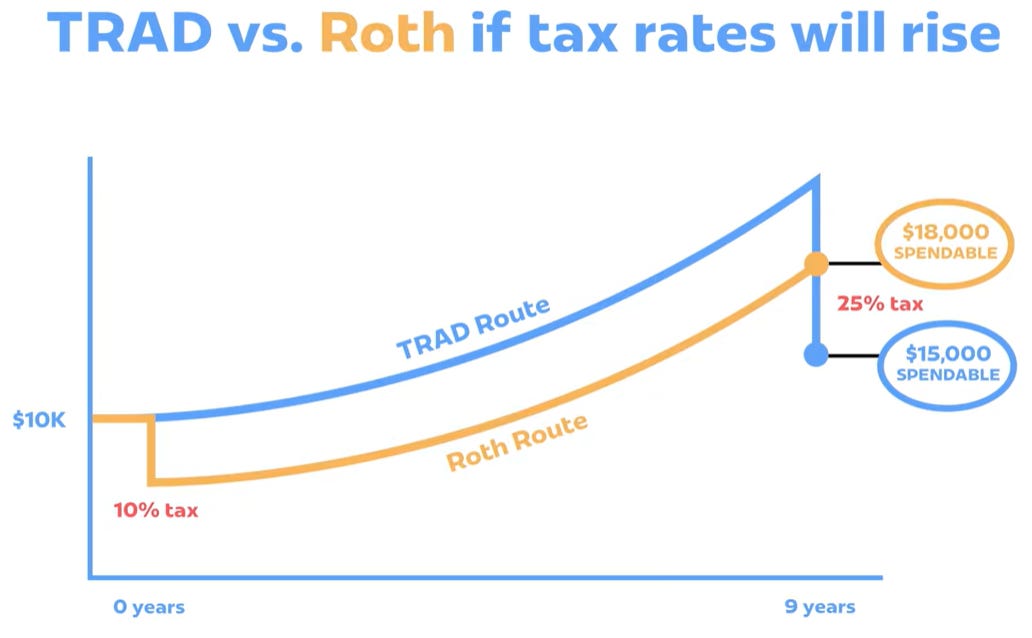

1. Your tax rate will rise.

If you are early in your career, in a low-income year, or you expect to have more taxable income in retirement, pay the taxes now. Go Roth. You win when the rate goes up.

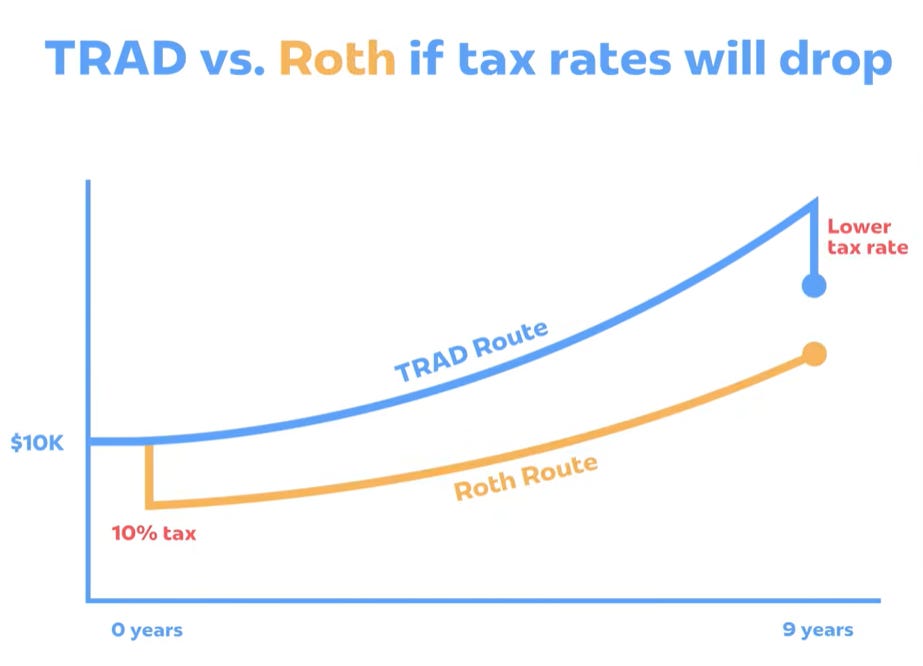

2. Your tax rate will drop.

I was working with a physician who was making $500,000 to $600,000 a year, sitting in about a 30% federal tax bracket. He was making Roth contributions. But this couple planned to spend about $80,000 a year in retirement. Their effective tax rate in retirement was going to be somewhere around 10 to 12%. He was paying taxes at 30% to avoid taxes at 12%. That is the wrong call. Traditional made more sense. And notice, none of that had anything to do with what the government decides to do with tax rates. That was entirely about his own situation.

3. You want to max fund your contribution limits.

This one changes how you think about the balance sitting in your retirement account. If you put $23,500 into a traditional 401(k), some of that money already belongs to the IRS. You just do not know it yet. I like to say you are in a partnership with the IRS on traditional money. The split is your tax rate. Put $23,500 into a Roth 401(k) and 100% of that is yours. Every dollar. So max-funded Roth contributions are worth more than max-funded traditional contributions at the same contribution limit.

4. You want degrees of freedom.

An engineer taught me this term. Degrees of freedom means you are setting yourself up so that in the future you have options, not just one path. If all your retirement money is in traditional accounts, every dollar you spend is a taxable event. But if you have a mix of traditional, Roth, and non-retirement brokerage accounts, you can pull from different sources based on what the tax environment looks like in any given year. You can stay in a lower bracket. You can realize capital gains at 0%. You can avoid Medicare surcharges. It is like sitting in front of an airplane cockpit with a lot of levers to pull.

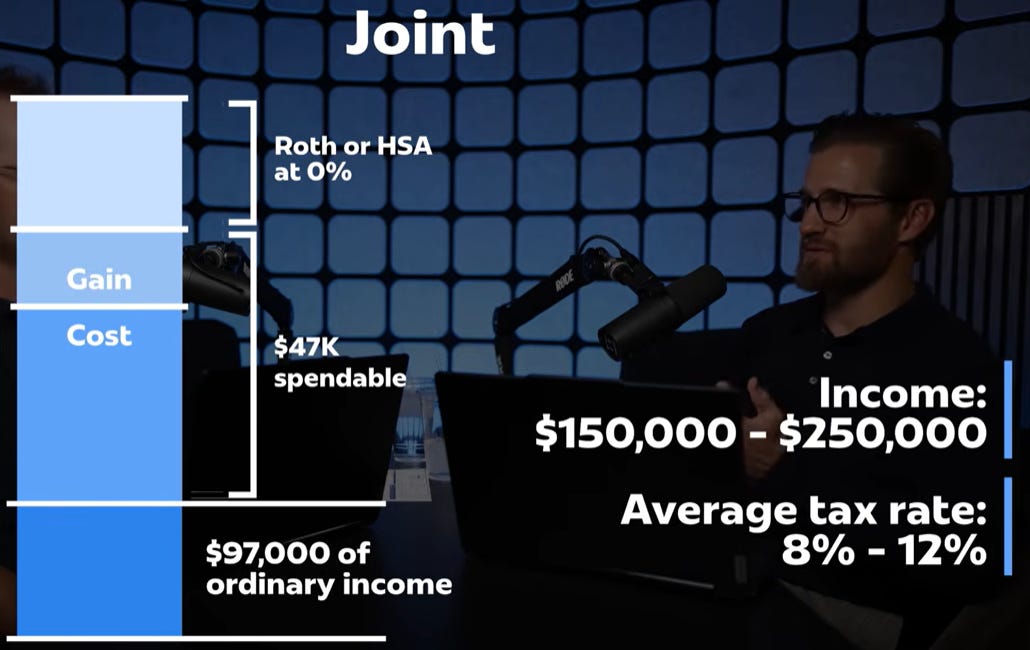

Here is what retirement taxes look like for a well-prepared couple. Social Security comes in. Much of it is taxed at a low rate or not at all, depending on your other income. A pension or rental income stacks in at the 10 and 12% brackets. Then there is headroom. You can pull traditional IRA money at 12%. You can harvest long-term capital gains at 0%. You can draw from Roth or an HSA with zero tax cost. A couple with $150,000 to $250,000 of annual income in retirement might have an effective federal tax rate of 8 to 12%. That is not a tax nightmare. That is a well-structured plan.

If you want to go deeper on any of these, I cover all of it step by step on my YouTube channel at https://www.youtube.com/@ZaccMoneyEducation.

What You Are Being Sold

There is a financial services presentation I have seen more than once where an advisor puts a $5 bill, a $10 bill, and a $20 bill on the table and asks a client which one they want to pay taxes on. The client picks the $5. Then the advisor sells them on whatever product lets them avoid taxes later.

The problem is that the math only works if your tax rate changes. If your rate stays the same, it does not matter which bill you picked. And if your rate drops in retirement, which it often does, you may have been better off going the other direction the whole time.

I have also seen this framing from well-known financial personalities online. The claim is that traditional only beats Roth if your tax rate drops dramatically in retirement. That word dramatically is just not accurate. Even a 1% difference in your favor matters. You do not need a dramatic drop to win with traditional. You just need a drop.

The reason this kind of advice gets amplified is not because it is right. It is because fear gets people to pick up the phone. My goal this season is the opposite of that. Be aware of taxes. Not afraid of them.

The mailers that say you will lose 70% of your IRA to taxes? I ran the math on that. To make it work, you would need over $30 million in assets, income over approximately $700,000 a year, a large taxable estate at death, and heirs also earning over approximately $700,000. That applies to a vanishingly small fraction of the population. For everyone else, retirement taxes are manageable. You just need to plan for them.

Where We Go From Here

This episode is the foundation. If you understand that the Same Spendable principle is real, and that tax rate differences are the only thing that actually changes the outcome, you are ready for what comes next.

In Episode 2, Tyson Long, one of our senior wealth advisors at Capita, and I will walk through eight advanced reasons to go Roth or traditional. Required minimum distributions, Medicare Part B premiums, Social Security taxability, and more. The nuances that matter for people with more complex situations or those getting closer to retirement.

You can follow the full Season 2 playlist here:

The goal of this entire season is straightforward. You understand Roth. For real. Not in a way that someone sold you on. In a way that lets you make the right call for your own situation.

This is the Season 2 outline:

This is Season 2, Episode 1 of The Guided Path. You can watch the full episode here:

And if you have a question about which direction makes sense in your own situation, my team and I work through exactly these decisions with people every day. You are welcome to reach out.

Click here to learn more about Capita.

Zacc Call, CFP® President & Managing Partner, Capita Financial Network

© 2026 Capita Financial Network. All rights reserved. All information provided through Education is for educational purposes only and does not constitute investment, legal or tax advice, an offer to buy or sell any security or insurance product; or an endorsement of any third party or such third party’s views. Whenever there are hyperlinks to third-party content, this information is intended to provide additional perspective and should not be construed as an endorsement of any services, products, guidance, individuals or points of view outside Capita Financial Network. All examples are hypothetical and for illustrative purposes only. Please contact us for more complete information based on your personal circumstances and to obtain personal individual investment advice. Capita Financial Network does not offer tax or legal advice. Interested parties are strongly encouraged to seek advice from qualified tax and/or legal experts regarding the best options for your particular circumstances. Videos presented on this website are for educational purposes only and do not constitute investment advice or an offer to buy or sell any security or insurance product. © 2026 All advisory services offered through Capita Financial Network, a SEC registered investment advisor. Registration with the SEC does not imply certain training or skill. Results are not guaranteed.

Hi Zacc, really enjoyed your piece. What is your perspective on backdoor Roth conversions?